Understanding Negative Equity: Negative equity occurs when you owe more on your car loan than the vehicle is worth. This affects about 11.6% of vehicle loan originations according to the Consumer Financial Protection Bureau. At Team Kia of Bend, we help customers navigate this financial challenge with strategic options including refinancing, making additional payments, or trading in with specialized financing solutions.

Ever thought you might owe more on your car than it’s worth? This is a common problem for millions of drivers in the U.S.

Vehicle equity is the difference between what you owe on your car and its current market value. If you owe more, you’re “underwater” on your loan.

Consumer Financial Protection Bureau (CFPB) data shows that 11.6% of vehicle loan originations between 2018 and 2022 involved borrowers rolling negative equity into the new loan. With about 114 million auto-loan accounts in the U.S. – representing roughly 64 million unique borrowers – you’re not alone.

But there’s hope. At Team Kia of Bend, we help customers deal with these tough financial situations. Knowing about depreciation, loan terms, and market conditions can guide you forward.

What Is Negative Equity on a Car and Why It Occurs

Negative equity happens when you owe more on your car loan than the car is worth. This is a tough spot to be in, affecting your choices when selling or trading your vehicle. The Federal Trade Commission explains this clearly.

It’s like being in debt on a mortgage but with a car instead. The math is simple, but the effects can be complex. An auto loan calculator with negative equity shows how much you’re in the red.

Understanding Vehicle Equity and Loan Balance

Vehicle equity is like home equity but for cars. It’s the car’s market value minus what you still owe. If it’s positive, you have equity. If it’s negative, you’re underwater.

For example, if your car is worth $15,000 but you owe $18,000, you’re $3,000 underwater. This means you’d need an extra $3,000 to break even if you sold it today.

The Consumer Financial Protection Bureau found that those with negative equity had bigger loans. They averaged $32,316 compared to $26,767 for those without a trade-in. This shows how big loans can lead to longer payback times.

Common Reasons You End Up Underwater on Your Auto Loan

Several factors can lead to negative equity. Making a small or no down payment is a big one. Financing the full purchase price means you owe more than the car’s worth.

Long loan terms also contribute to this issue. While they lower monthly payments, they slow down paying down the principal. Early on, most of your payment goes to interest, not principal.

Rolling previous negative equity into a new loan makes things worse. If you traded in a car with $2,000 negative equity and added it to a $25,000 loan, you owe $27,000 on a $25,000 car. A car loan calculator with negative equity can show how this affects your payments.

Purchasing vehicles that depreciate quickly also leads to underwater loans. Luxury cars, certain brands, and vehicles with poor reliability ratings lose value fast.

How Rapid Depreciation Creates Negative Equity

New cars lose a lot of value right after you buy them. They can depreciate 20-30% in the first year alone. This loss often exceeds what you’ve paid toward your loan principal.

Market conditions can make depreciation worse. Economic downturns, changes in fuel prices, or shifts in consumer preferences can cause certain vehicles to lose value quickly. The 2020-2022 period showed how unusual market conditions can affect car values.

Different vehicle types depreciate at different rates. Sports cars and luxury vehicles depreciate faster than practical sedans or popular SUVs. Knowing this helps you make better decisions about loan terms and down payments.

Understanding these patterns helps you avoid problems. Using tools like a car payment calculator with negative equity before buying can show you potential scenarios. This helps you avoid trouble from the start.

How Negative Equity Impacts Your Financial Situation

Negative equity affects more than just your car payments. It impacts your whole financial situation. Knowing this helps you make better choices for your vehicle and finances.

Being upside down on your car loan can hurt your credit and limit your options. But, knowing the problems early can help you tackle them better.

Effects on Your Credit Score and Borrowing Power

Does negative equity hurt your credit score? It’s not that simple. Negative equity itself doesn’t lower your credit score.

But, it can have big indirect effects. Your payments might take up too much of your income. The Consumer Financial Protection Bureau found that those with negative equity paid 9.8% of their income on their car, compared to 7.7% for those with positive equity.

This can lead to missed payments or default. The CFPB also found that those with negative equity were more than twice as likely to have their cars repossessed within two years.

Your ability to borrow money also suffers. Lenders don’t like high debt-to-income ratios. Those with negative equity had an average credit score of 704, while those with positive equity had 752.

Challenges When You Want to Trade In or Sell

Selling a car with negative equity is tough. You can’t just walk away from the loan. You still owe the difference, even if the car’s value has dropped.

When trading in, the dealer will pay off your loan, but you must cover the gap. This can cost hundreds or thousands of dollars, depending on how much you owe.

Private sales face similar issues. Even if you sell your car for fair market value, you still owe the difference. This can surprise car owners, making it hard to sell quickly.

The timing of a sale is also important. Market conditions, the season, and your car’s condition affect its value. These factors rarely match your selling schedule.

Understanding Your Options When Moving Forward

Despite the challenges, you have options for a car with negative equity. It’s important to understand each option’s pros and cons.

Some choose to keep their car and pay extra to build equity. Others trade in, even with negative equity, by rolling the difference into a new loan. Each choice has different financial effects and timelines.

If you’re looking to escape negative equity, refinancing might help if your credit has improved. Some lenders offer better terms that can lower your payments or shorten your loan.

Getting rid of negative equity takes time. Keep making payments and your car’s value will increase. Market conditions can also help, depending on your car’s type.

The key is to avoid making hasty decisions. Negative equity is temporary and can be overcome with the right plan. Working with experienced dealerships and advisors can guide you through this.

Remember, you’re not alone. The automotive finance industry has solutions for negative equity. Your situation may seem tough, but it’s not hopeless.

Smart Strategies for Handling Your Upside Down Car Loan

Being upside down on your car loan doesn’t mean you’re out of options. The FTC warns about dealers rolling negative equity into new loans, but smart strategies can help. You can manage this challenge effectively.

Financing negative equity can cost you a lot. In the CFPB’s 2018-2022 sample, new-car buyers had to pay an average of $5,073 extra on their loan in rolled-in negative equity, and used car buyers paid an average of $3,284. In 2022, 13% of new-car buyers in the $20,000-$29,999 range financed negative equity. You’re not alone in this situation.

Trading In Your Vehicle Despite Negative Equity

To trade in a car with negative equity, start by getting multiple appraisals. Visit different dealerships and use online tools. An independent appraisal can also help you understand your car’s value.

Dealers add the negative equity to your new loan. For example, if you owe $25,000 but your car is worth $20,000, you’ll carry the $5,000 difference. Negotiating a good trade-in value is crucial.

Timing your trade-in wisely can help minimize losses. Avoid trading during the first two years when your car’s value drops a lot. Try to wait until your loan balance is closer to your car’s value.

Dealerships that handle bad credit can help with negative equity. They often have lenders who understand these situations.

Rolling Negative Equity into a New Kia Lease or Purchase

Rolling over negative equity into a new vehicle needs careful planning. Choose vehicles with strong resale values and short loan terms to build equity faster.

A negative equity lease can be appealing because lease payments are often lower. But, rolling $20,000 into a lease means you’ll pay for it without building ownership. Use a lease calculator to understand your costs.

Kia vehicles are good for negative equity situations. They have strong warranties, competitive financing, and good resale values. Team Kia of Bend helps customers with negative equity car deals.

Choose reliable vehicles with good track records when rolling over negative equity. This ensures your new car keeps its value better than your old one.

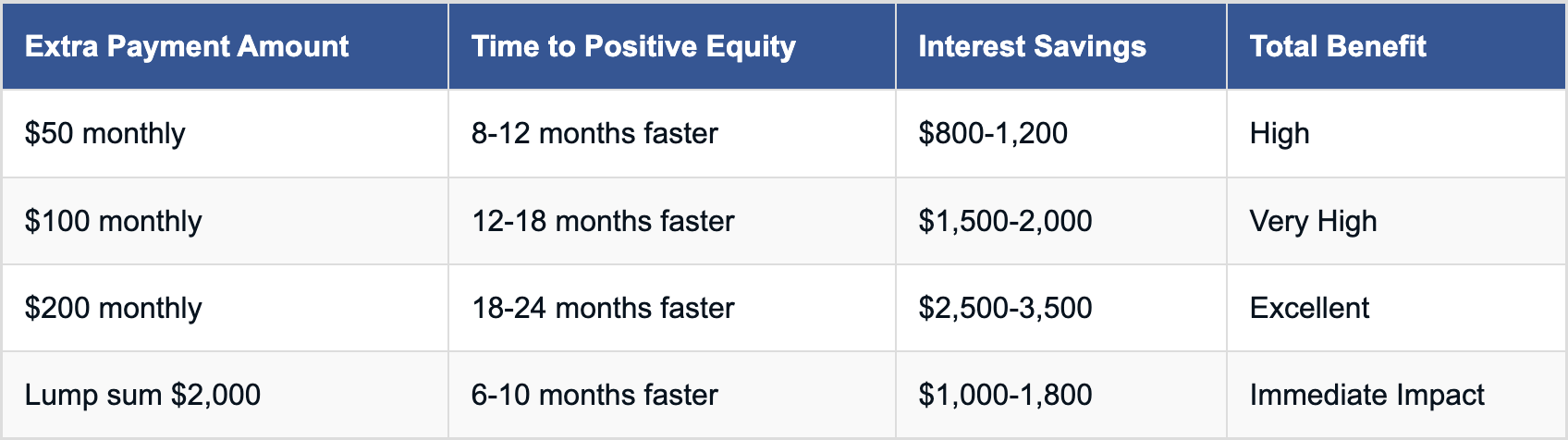

Making Additional Payments to Build Positive Equity

Making extra payments is often the best way to handle negative equity. Even small extra payments can cut down the time to reach positive equity.

Target your extra payments to the principal balance, not the regular payment. This reduces what you owe without extending your loan term.

Find money for extra payments by cutting unnecessary expenses. Use tax refunds, bonuses, or side income for loan principal reduction.

Check your loan balance against your car’s value monthly. This helps you see the results of your extra payments.

Finding Dealerships That Work with Negative Equity Situations

Dealerships that accept negative equity know how to protect your finances. They understand how to get you a new car with negative equity while minimizing risks.

Ask dealers about their experience with underwater loans. Experienced dealers can offer creative financing solutions and work with multiple lenders for the best terms.

Team Kia of Bend specializes in negative equity situations. We provide clear guidance and work with customers to create solutions that fit their budgets and goals.

Choose dealerships that explain all costs and terms clearly. Avoid those who pressure you or are not transparent about handling negative equity.

Ask dealers about their lender relationships. Good relationships mean better financing options and more flexible terms for your situation.

Conclusion

Dealing with negative equity on your car doesn’t have to feel overwhelming. You now understand the causes and have learned practical strategies to address your upside down car loan situation. The key is taking action rather than avoiding the problem.

Industry data shows that working with knowledgeable dealerships helps consumers navigate negative equity situations more effectively. Professional guidance can prevent future financial complications and open doors to solutions you might not have considered.

At Team Kia of Bend, our experienced finance team understands the complexities of negative equity situations. We work with customers daily to explore all available options, from trade-in strategies to rolling equity into new vehicle purchases. Our goal is helping you find the best path forward for your specific circumstances.

Your negative equity situation is temporary. With the right approach and professional support, you can overcome this challenge and get back on track financially. The first step is reaching out to discuss your options.

Visit Team Kia of Bend at 611 NE Purcell Blvd, Bend, OR 97701, or call 541-550-5555 to speak with our finance specialists. We’re here to help you navigate your auto loan challenges and find solutions that work for your budget and lifestyle.

FAQ

How do you get negative equity on a car?

Negative equity often comes from quick car depreciation and loan terms that don’t match the value loss. It can happen if you make a small down payment, choose long loan terms, or buy during market peaks.

Does negative equity affect your credit score?

Negative equity itself doesn’t directly hurt your credit score. But, the financial stress from high payments or the risk of default can harm your credit. As long as you pay on time, your score should stay good.

Can you trade in a car with negative equity?

Yes, you can trade in a car with negative equity. The negative equity amount will likely be added to your new loan, making your payments higher. It’s key to work with dealerships that know how to handle these deals well.

Can you roll negative equity into a lease?

Yes, you can roll negative equity into a new lease, which will raise your monthly payments. Leasing can be a smart choice for managing negative equity, if you pick a vehicle with strong residual values and short terms.